Reasons To Retain Abbott Stock In Your Portfolio For Now

Strong momentum in Abbott Laboratories' ABT Nutrition business is expected to support growth in the coming quarters. The company is driving solid growth in emerging markets within the Established Pharmaceuticals Division (“EPD”) business. However, currency fluctuations and dull macro scenario may restrict Abbott’s growth potential.

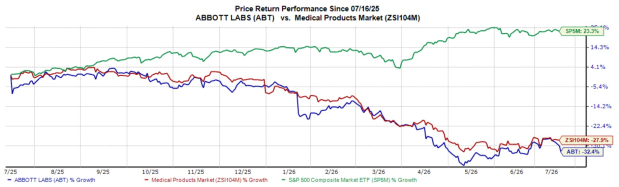

In the past year, this Zacks Rank #3 (Hold) company’s shares have lost 32.4% compared with the industry’s 27.5% decline. The S&P 500 composite has risen 23.3% in the same period.

The leading at-home healthcare company has a market capitalization of $228.81 billion. Abbott beat on earnings in two of the trailing four quarters and matched in the other two, delivering an average surprise of 0.42%.

ABT’s Tailwinds

EPD Momentum Across Emerging Markets: Abbott’s EPD remains a steady contributor, supported by branded generics positions in faster-growing geographies. In the first quarter of 2026, EPD sales increased 13.2% on a reported basis and 9.0% on a comparable basis, with Key Emerging Markets up 9.4% on a comparable basis led by double-digit growth in several countries across Latin America and Asia Pacific.

The company continues to focus on demand drivers such as chronic disease prevalence and expanding access to care, which support durable volume growth across therapy areas. It is also expanding its biosimilar portfolio, which should deepen its offering in key markets and help sustain above-market growth as the business scales.

Innovation-Led Reset in Nutrition: Abbott is working through a transition in Nutrition that is intended to restore a healthier balance between price and volume over time. In the first quarter of 2026, Nutrition sales declined 6.0% on a reported basis and 7.7% on a comparable basis, reflecting lower volumes and the impact of strategic pricing actions taken in the fourth quarter of 2025. Adult Nutrition remains an important franchise within the portfolio and a more consistent cadence of innovation, which should help it defend brand positions as category conditions normalize.

Image Source: Zacks Investment Research

What Ails ABT Stock?

Macro and Cost Variability: Abbott continues to operate amid an uncertain macro backdrop that can influence input costs and demand patterns across categories. In the first quarter of 2026, selling, general and administrative expenses increased 22.2% year over year, partly reflecting acquisition-related items, and the company continues to incur incremental costs tied to European MDR and IVDR compliance. If pricing, mix or volumes weaken in areas such as Nutrition, Abbott may have less flexibility to offset these costs, which could weigh on profitability even with ongoing cost actions.

Foreign Exchange Can Swing Reported Results: Abbott’s large international revenue base makes reported growth sensitive to currency translation. Any reversal in currency trends would quickly reduce reported growth rates and complicate comparisons against expectations.

Abbott’s Estimate Trend

The Zacks Consensus Estimate for 2026 earnings per share has remained unchanged at $5.48 in the past 30 days.

The Zacks Consensus Estimate for 2026 revenues is pegged at $50.42 billion, indicating a 13.7% rise from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Globus Medical GMED, Integra LifeSciences IART and Phibro Animal Health PAHC.

Globus Medical has an earnings yield of 5.5%, well ahead of the industry’s negative 3% yield. Its earnings surpassed estimates in each of the trailing four quarters, the average surprise being 26.3%. The company’s shares have rallied 43.8% against the industry’s 4.8% decline over the past year.

GMED carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Integra LifeSciences, carrying a Zacks Rank #2 at present, has an earnings yield of 16% against the industry’s negative 3% yield. Shares of the company have gained 22.8% compared with the industry’s 4.8% growth. IART’s earnings topped estimates in each of the trailing four quarters, the average surprise being 16.8%.

Phibro Animal Health, carrying a Zacks Rank #2 at present, has an earnings yield of 9.2% compared with the industry’s 2.8% yield. Shares of the company have climbed 43.1% against the industry’s 27.9% decline. PAHC’s earnings beat estimates in each of the trailing four quarters, the average surprise being 16.3%.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).

Popular Products

-

Automotive CRP123X OBD2 Scanner Tool

Automotive CRP123X OBD2 Scanner Tool$649.56$324.78 -

Portable USB Rechargeable Hand Warmer...

Portable USB Rechargeable Hand Warmer...$61.56$30.78 -

Portable Car Jump Starter Booster - 2...

Portable Car Jump Starter Booster - 2...$425.56$212.78 -

Electric Toothbrush & Water Flosser S...

Electric Toothbrush & Water Flosser S...$43.56$21.78 -

Foldable Car Trunk Multi-Compartment ...

Foldable Car Trunk Multi-Compartment ...$329.56$164.78