Hazel Plans To Take Cpp And Oas But Is Worried About Having Enough In Retirement. Does Buying An Annuity Make Sense?

Q. I’m a 62-year-old divorced human resource manager and earned $120,000 a year before I retired last year. I have been living off a small $85,000 inheritance. I’m a bit worried as I have no company pension so I will need to start drawing down my investment portfolio later this year and I am concerned that I won’t have enough money. I know I can return to work if I have to but I don’t really want to. Will my money last my lifetime?

Right now, my assets include $222,400 in a registered retirement savings plan (RRSP), $40,000 in a tax-free savings account (TFSA) and $269,000 in a locked-in retirement account (LIRA), for total investments of $531,400. I am invested 50 per cent in fixed income, 30 per cent in Canadian equity, 10 per cent in U.S. equity, eight per cent in international equity and two per cent in cash. I also have a paid-off condo worth $460,000. I need $45,000 annually to live comfortably and that includes all condo fees, taxes, travel money, gifts for my children and grandchildren, as well as other discretionary spending.”

To stretch my savings, I have considered going back to work part time or doing a bit of contract work but I don’t really want to. Instead, I plan to take Canada Pension Plan (CPP) — 90 per cent of the full amount — and Old Age Security (OAS) at age 65 to avoid any penalty. My investment returns have averaged three per cent net after fees, but I wonder if buying an annuity with some of my investment money would make sense. I want to sleep at night. Before I finally leave work and drop all my contacts, I want to make sure I have a plan in place that will give me a comfortable retirement that will last a lifetime. —Hazel H.

FP Answers: Hi Hazel, let’s do a little scenario planning and look into your future. Then you will be in a much better position to make good financial decisions today.

You have given me most of the information I need to run some simple scenarios, and I will assume you are in Ontario and your CPP at age 65 will be $16,000 a year.

The first step is to benchmark your current situation so we can measure against any changes we make in different scenarios. It will also allow us to double check and question some of your assumptions.

I have you converting your LIRA to a Life Income Fund (LIF) now and transferring 50 per cent of the value of your LIRA to your registered retirement income fund (RRIF), as is permitted in Ontario. CPP and OAS are starting for you at age 65 and you are living on $45,000 a year after tax, indexed at two per cent to age 90. In that scenario your investments dwindle down to $12,500 in today’s dollars by age 90 and your after-tax estate value is about $608,000. You have worked it out perfectly, but we need to question a few things, starting with your income.

Is $45,000 a year after tax enough? You were earning $120,000 a year at your job, leaving you about $91,500 after tax, a difference of about $46,000, for simplicity. If you were maximizing your RRSP contributions you would have $77,700 after tax, still a big difference. Be careful saying you can live on a certain amount of money unless you really know you can. It is a big risk underestimating your retirement spending. What are you willing to give up? Try writing out your expenses as a double check.

If you spend an extra $5,000 a year, which doesn’t seem like much, you will start running shy of money by age 77. Your RRIF and TFSA will be gone, and your income sources will be your CPP, OAS and the maximum LIF payments. You will still have equity you could use in your condo if you are comfortable using it by selling or borrowing against it.

- Can Valeria, 53, with investments worth $1 million in RRSPs, TFSAs and GICs, retire in two years?

- Is Caesar, a 37-year-old renter, putting too much money into retirement savings and employee stock?

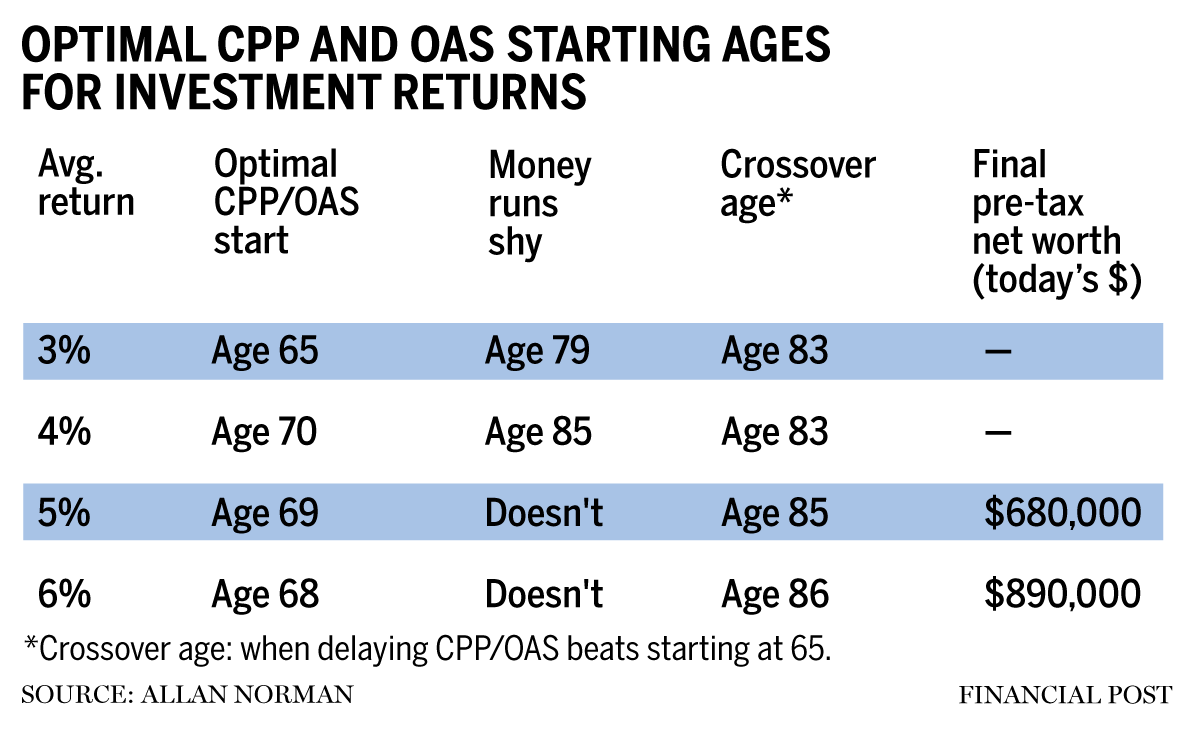

On your annuity question, rather than purchasing an annuity, think about delaying CPP and OAS, which is effectively buying an annuity. One deciding factor in when to start CPP and OAS is the rate of return you expect to earn on your investments. The accompanying chart models four scenarios, all assuming you start CPP and OAS at the optimal age for each return rate.

You can see from the table that a conservative return likely means you cannot rely only on your investments if you want to maintain an income of $45,000 a year. A little part time-work earning just $10,000 a year for the next four years can have a big lifetime impact. Your final pre-tax net worth will go from $680,000 to $772,000 in the plan with you earning five per cent and starting CPP and OAS at age 69.

Hazel, be careful. You are riding the edge here and your conservative mindset may not lead to a sleep-easy retirement. You may also find that you are spending and living less than you actually can for fear of running out of money. If you have an easygoing personality and you are sure $45,000 a year after tax is the right figure, you may be okay. But if you are a worrier I would consider the part-time or contract work, at least for a few years. A little work early in retirement buys a lot of peace of mind later.

Allan Norman, M.Sc., CFP, CIM, provides fee-only certified financial planning services and insurance products through Atlantis Financial Inc. and provides investment advisory services through Aligned Capital Partners Inc., which is regulated by the Canadian Investment Regulatory Organization. He can be reached at alnorman@atlantisfinancial.ca.

Do you have a question for FP Answers? Email wealth@postmedia.com.

Popular Products

-

Devil Horn Headband

Devil Horn Headband$25.99$11.78 -

WiFi Smart Video Doorbell Camera with...

WiFi Smart Video Doorbell Camera with...$61.56$30.78 -

Smart GPS Waterproof Mini Pet Tracker

Smart GPS Waterproof Mini Pet Tracker$59.56$29.78 -

Unisex Adjustable Back Posture Corrector

Unisex Adjustable Back Posture Corrector$71.56$35.78 -

Smart Bluetooth Aroma Diffuser

Smart Bluetooth Aroma Diffuser$585.56$292.87