The Government Is Trying To Rein In Medicare Advantage Costs. Will It Work?

Keeping healthcare costs under control is crucial for retirees.

Something good recently happened. The Centers for Medicare and Medicaid Services (CMS) announced that its proposed average increase for 2027 in the rates that Medicare pays insurers for Medicare Advantage plans is projected to be only 0.09 percent. Analysts had predicted that the 2027 rate increase would be roughly in the range of 4 percent to 6 percent, in line with the 5.06-percent increase insurers enjoyed in 2026.

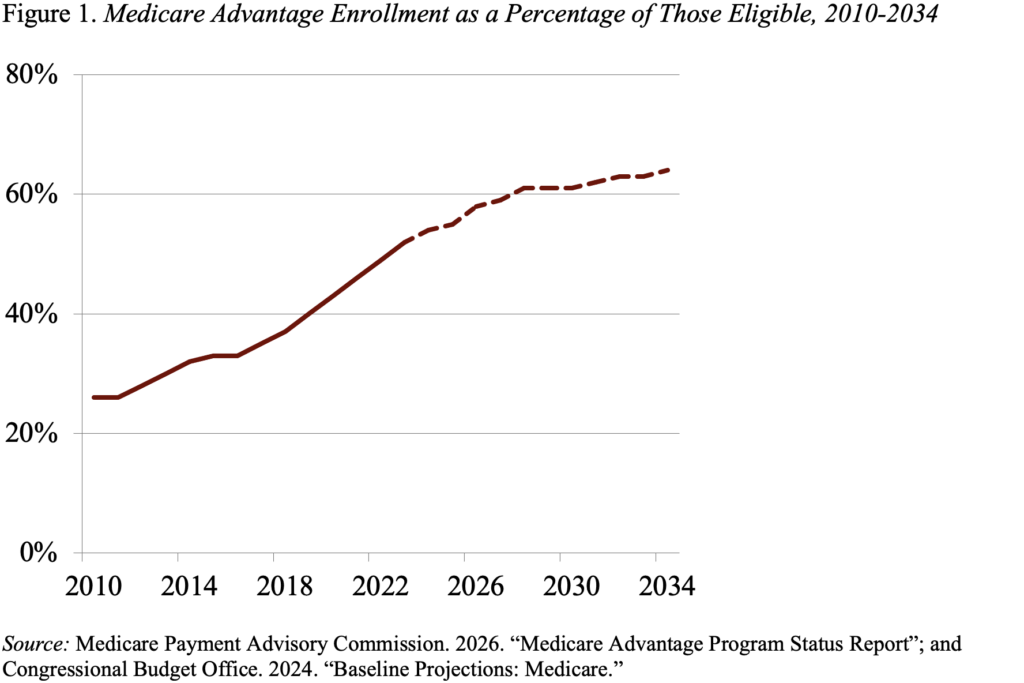

This proposal is a big deal because Medicare Advantage plans are a big deal. In 2025, more Medicare participants received their benefits through a Medicare Advantage plan offered by a private insurer rather than through government-run traditional Medicare, a share that is projected to continue rising over time (see Figure 1).

People gravitate towards Medicare Advantage plans for three reasons: 1) enhanced benefits, such as dental, vision, hearing, and fitness; 2) a limit on annual out-of-pocket costs for Part A and B services (unlike traditional Medicare); and 3) low or zero premiums. In return, enrollees must accept the plans’ procedures, such as prior authorization for accessing care, and more limited networks of health care providers. On balance, however, it’s clear why older people often opt for Medicare Advantage plans.

The big problem, however, is that Medicare Advantage plans are really expensive for Medicare. Congress’s Medicare Payment Advisory Commission estimates that payments for Advantage beneficiaries in 2025 were 20 percent higher than for traditional Medicare. While Medicare usually pays for services that participants actually receive, the program pays Medicare Advantage plans a fixed amount per enrollee. That amount is tied to local benchmarks, higher for plans with higher ratings, and risk-adjusted to reflect the health status of each plan’s enrollees.

Because Medicare Advantage plans receive higher payments for less-healthy enrollees, insurers have an incentive to identify as many health conditions as possible for each enrollee. Not surprisingly, Medicare Advantage plans record more health conditions than traditional Medicare for comparable beneficiaries.

Analysts attribute this pattern, at least in part, to “chart reviews,” which insurers use to determine whether the individual’s medical records are consistent with the info submitted by the provider. While chart reviews could identify an additional factor that could impact a person’s health status, they can also identify diagnoses that are inaccurate, no longer active, or unrelated to the clinical care and therefore not relevant for payment purposes. In 2022, 62 percent of MA enrollees had a chart review, and these reviews were significantly more likely to add a diagnosis than remove one.

CMS’s announcement to hold steady 2027 payments to Medicare Advantage plans reflects the agency’s plan to update its risk adjustment model to better reflect current costs. A key part of that effort involves excluding from the calculation diagnosis information from chart reviews that is not associated with a specific beneficiary encounter.

CMS will accept comments on the proposed payment increase through February 25, 2026, before publishing its final rate increases on or before April 6, 2026. Clearly, this decision will have the largest impact on the companies that have relied the most extensively on chart reviews (see Table 1).

CMS has taken a bold step; let’s hope the agency sticks with it. Keeping health care costs under control is crucial for the economic security of current and future retirees.

Popular Products

-

Adjustable Shower Chair Seat

Adjustable Shower Chair Seat$107.56$53.78 -

Adjustable Laptop Desk

Adjustable Laptop Desk$91.56$45.78 -

Sunset Lake Landscape Canvas Print

Sunset Lake Landscape Canvas Print$225.56$112.78 -

Adjustable Plug-in LED Night Light

Adjustable Plug-in LED Night Light$61.56$30.78 -

Portable Alloy Stringing Clamp for Ra...

Portable Alloy Stringing Clamp for Ra...$119.56$59.78