The New American Dream: Owning Just Part Of A Home

Getty Images; Tyler Le/BI

If you're looking to buy a house, odds are you'll spend more time scrutinizing the four walls than the ground underneath. There's a good chance, however, that most of your dollars will go toward paying for that land. In the Los Angeles metro, for instance, land often accounts for well over 60% of a single-family home's total value. A pricey patch of dirt can put homeownership out of reach for even the most scrupulous savers. Jubilee Homes, a San Francisco-based startup, proposes an unorthodox alternative: What if you could buy the house without the land?

So-called "leaseholds" are common in countries like the UK and Singapore, where residents can buy a house for a lower price and rent the underlying land from the government or a corporation. In the US, some nonprofits use leaseholds to prevent property prices from spiraling out of control — at Stanford University, for example, many professors own their homes but lease the land from the university for a modest fee. Still, the practice remains niche here, and it's rare for private companies to provide such a deal.

Enter Jubilee, which offers cash-strapped homebuyers its own spin on leaseholds. The company is part of a growing web of "fractional ownership" startups that aim to add a few rungs to the property ladder, making homeownership feasible for more Americans while also making a buck for themselves and their investors. The flavors of these deals vary, but the formula is roughly the same: A company partners with a regular homebuyer on their purchase, taking a stake in the property — often a large one — and sharing in the upside. These companies pitch themselves as alternative on-ramps to homeownership, helping Americans bridge the yawning gap between renting and building wealth in a place they can call their own.

Not everyone is buying into their promise. "If it sounds too good to be true, it usually is," says Sharon Cornelissen, the director of housing for the Consumer Federation of America. People who sign on to these deals may not understand the precise financial tradeoffs, Cornelissen tells me, or they may wind up bearing the burden of ongoing homeownership costs — maintenance, insurance, property taxes, etc. — while investors enjoy most of the upside.

"It's so difficult to get into homeownership right now, I expect we'll see a growing space for this kind of process," Cornelissen says. "But at any time, consumers should be sort of skeptical about it."

As both sides of the political aisle take shots at corporate landlords, leaders of companies like Jubilee say that their products offer a rare win-win: profits for investors, sure, but also a path to homeownership for millions of renters. The American dream 2.0? Maybe. But to fulfill that promise, this crop of companies will have to prove they offer more than just the illusion of true ownership.

On a rainy morning in early March, I met Jubilee's CEO, Brian Elbogen, at a café in Manhattan's Financial District, where he told me about the first time he bought a house. It was a decade ago in San Francisco, and Elbogen and his wife had already lost out on several homes in the city's notoriously competitive market. They decided to try a different tack: Rather than brave another bidding war on their own, they went in on a three-unit building with two other families. Sorting out the financing and legal details was a "cockamamie-like process," Elbogen told me. "But you know what it did? It got us in the door."

Elbogen and his wife have since moved, but his first taste of fractional ownership stuck with him. The way he sees it, housing choice in America is too often reduced to a frustratingly binary decision: "You can either own nothing, or you can own everything." Renting puts a roof over your head, but it won't do much for you in the way of wealth-building. The other option is to buy a house, but that requires saving up tens of thousands of dollars for a down payment and going hat-in-hand to a mortgage lender.

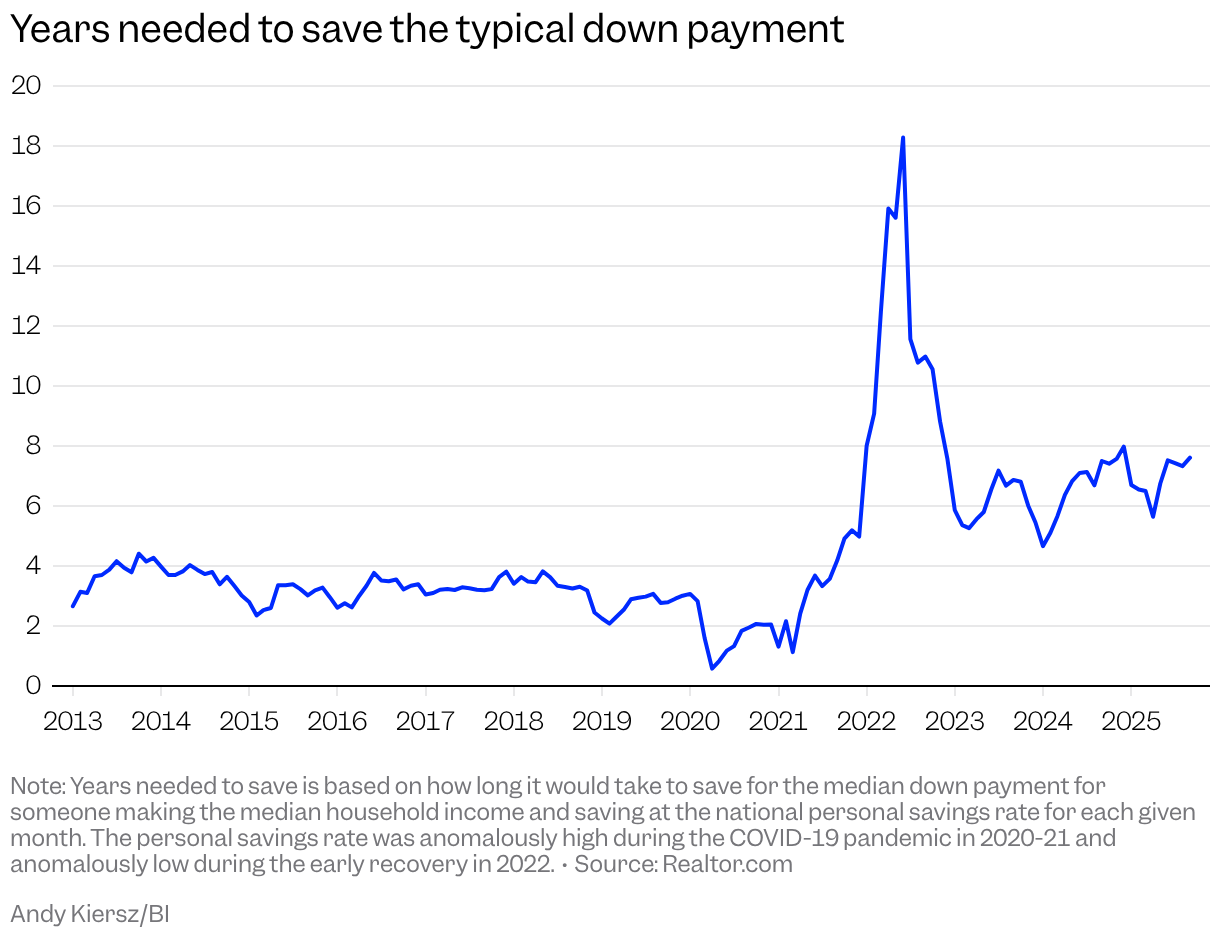

The barrier to entry is steep. In the third quarter of last year, the typical down payment was $30,400, Realtor.com found. For a household earning the median income and saving the average amount, it would take seven years to save up that money — double the pre-pandemic norm.

In other countries, there's often a third option: part renting, part owning. In the UK, it's called "shared ownership"; in Norway, "deleie bolig." While the details "might differ to some degree, the general idea of having this hybrid product" is the same, says Marlene Koch, an economist at Maastricht University in the Netherlands who studies housing finance. The occupant of the house owns part of it and pays monthly rent on the rest to a separate investor. The occupant's stake may grow over time, and they may have the option to buy out the investor down the line. This model differs from "rent-to-own" companies, which typically encourage renters to save for a purchase by setting aside a portion of their monthly rent as a future down payment. Unlike the typical rent-to-own customer, fractional owners have a stake in the property from day one.

Fractional ownership often appeals to young, financially constrained individuals who might otherwise spend additional years renting, Koch tells me. Reaching homeownership earlier isn't the only potential benefit, though. When people pour the bulk of their savings into homebuying, they often ignore other wealth-building options, such as stocks or bonds. If they can get in with a lower down payment, or shave off some of their monthly payments through fractional ownership, they may be able to turn to other investments and, Koch tells me, reduce that "concentration risk in their portfolio."

If it sounds too good to be true, it usually is.Sharon Cornelissen, director of housing for the Consumer Federation of America

The finer details of fractional ownership vary starkly from one company to another. In Jubilee's case, this is how it works: Say you find a house you want to buy, but you can't afford the down payment, or you want lower monthly costs. You and Jubilee make a combined offer on the house — Jubilee purchases the land with cash, and you pay for the structure with a separate mortgage. Slicing up the purchase this way makes it vastly cheaper for you than buying the whole thing. Jubilee then offers you a 99-year lease on the land, for which you'll pay monthly rent in addition to your mortgage. The total monthly costs are lower or roughly comparable to a traditional purchase, the company says, and the required down payment shrinks dramatically. You can buy the land from Jubilee at any point for an amount determined by a third-party appraiser. Or, if you want to sell down the line, you can package the home and land together again, and Jubilee will get a cut of the total sales price. If the land accounted for 65% of the initial purchase price, the company will get 65% of the proceeds when it sells.

TWIG Media Lab, provided by Brian Elbogen

Leaseholds aren't the only way this can work, though. Other companies allow customers to start with a small stake in a home of their choice and build more equity over time. Consumers who work with Ownify, another San Francisco-based startup, can put down a mere 2% of the purchase price of their chosen house, and Ownify will cover the rest with cash. The occupant then makes a fixed monthly payment to Ownify, a portion of which goes toward buying more equity, or "bricks," in the property. Over time, the rent-to-bricks ratio shifts — in the later years of the agreement, a larger share of each monthly payment goes toward building equity in the property. The program lasts five years, by which time the consumer should own a roughly 10% stake, Ownify says. At that point, they can choose to either cash out, renew for another five years, or use that pile of equity to effectively take over the mortgage and own the place outright.

Zac Baker, an Ownify customer in Raleigh, North Carolina, says he and his partner began looking to buy a house in 2022 after years of steep rent hikes. Between his partner's student loans and Baker's own payments to support his family, they didn't have the money for a typical down payment, he tells me. After participating in a research group sponsored by Ownify, they began talking with some of the company's executives, who explained the process over a series of meetings. The company connected them with a real estate agent who helped them find a three-bedroom home for $355,000, which Ownify purchased in December 2022 (Baker and his partner paid $6,100 for a 2% initial stake). Because they agreed to the monthly payments at the outset, they know how much they'll be paying each month over the five-year agreement — no more annual increases. Ownify has also covered major plumbing repairs and an HVAC fix, which Baker describes as a "lifesaver at the time."

Baker says he and his partner are unsure what they'll do when the five years are up. Home prices have largely stagnated in Raleigh, so at this point, he's not looking at the kinds of wealth gains he'd hoped for when he first signed on. But he says the deal was still worth it to clear the initial hurdles.

"It's taking us longer to build equity in the home," Baker tells me. "But nonetheless, we know that we are building equity at the end of the day."

Mike Schneider, the cofounder and CEO of another startup called Acre Homes, says the current affordability crisis demands solutions beyond the 30-year mortgage. "People just haven't realized there's another alternative," he tells me. Acre doesn't quite fall under the fractional-ownership umbrella — customers aren't technically co-owners in the property — but it's another example of how companies are trying to mimic homeownership's wealth-building effects outside the typical purchase. Acre customers "buy in" to the program by paying 5% of the home's initial value to the company, which entitles them to lower monthly payments than a typical mortgage, plus half of the home's future appreciation over a five-year term. Acre also covers the transaction costs associated with buying and selling the property.

It's an appetizing deal for investors, too: Because the consumer gets part of the upside, they pay more each month than a typical renter. The Acre customer also covers the day-to-day expenses like utilities, property taxes, insurance, and minor maintenance (Acre covers big-ticket repairs). "Investors are getting a higher yield than if they just bought it and rented it out," Schneider says. Acre customers, he adds, "take great care of the home. There are aligned incentives."

The concept behind fractional-ownership companies is simple enough. The fine print is where things get tricky.

The past decade of housing history is littered with companies that tried and failed to usher in radical new approaches to homebuying. The US mortgage industry is a highly regulated, well-oiled machine — it's tough to break decades-old habits. The latest companies employ a wide range of setups and formulas to make the deals palatable for both consumers and investors. As far as I can tell, no two startups hit the exact same notes. Options are nice, sure, but the variety can make it hard to size up the deals and determine which, if any, is best. This problem isn't limited to the US. Even in countries with well-established markets for shared ownership, it can still seem like a "very abstract product," says Koch, the finance professor at Maastricht University.

"I spent years working on this, and still not everything is clear to me," Koch tells me.

I spent years working on this, and still not everything is clear to me.Marlene Koch, a housing economist at Maastricht University

Cornelissen, the director of housing for the Consumer Federation of America, says she also keeps a close eye on the fees associated with these kinds of deals. Some companies charge origination fees or annual upkeep fees, or leave the ongoing costs of homeownership to the resident. Jubilee customers, for example, are responsible for property taxes, insurance, utilities, and any community fees. Meanwhile, rent on the land increases by 3% each year: "This protects you from excessive rent increases while ensuring that Jubilee's investment keeps pace with inflation in the long run," the company explains in an info packet. Customers are also responsible for the closing costs associated with a sale, such as agent commissions, appraisal fees, and escrow fees, as they would be if they owned the place by themselves.

"What gives me pause is when investors have all the upside but not all the ongoing costs of maintaining the home and the monthly burden," Cornelissen tells me. "That's important, because there are a lot of costs that come with homeownership."

It may also be difficult for buyers to work out how much they're giving up when they take one of these deals. The companies' websites typically include sample scenarios or calculators to help customers compare the costs to those of a traditional mortgage and estimate how much equity they'll walk away with. But these calculations rely on a barrage of assumptions — stuff like loan-to-value ratios, estimated rent growth, mortgage rates, and annual home price appreciation. "If you've read this far, you're a rock star!" ends one such disclosure from Ownify.

Frank Rohde, the founder and CEO of Ownify, tells me "the math of homeownership is hard and confusing."

"The stance we've taken is to provide as much transparency, tools, and education as possible," Rohde says, noting that the company has posted 45 educational videos to YouTube, "and then let people self-educate as much as possible. If someone doesn't want to spend the time to learn and understand, or doesn't have the capacity to, then our product is probably not a good fit."

LifestyleVisuals/Getty Images

Any time investors try to get a piece of home-equity gains, there's bound to be pushback from those who fear Wall Street capital will crowd out humble homeowners. But we also lament when consumers bear all the potential downsides of ownership: ending up underwater on a mortgage, bearing sole responsibility for major repairs, or falling behind on expensive monthly payments.

"The honest answer is, you can't have it both ways," Rohde tells me. The logic of alternative models like his, Rohde adds, is that you can subsidize the homeownership journey by sharing in the upside and limiting the downside.

"If you think that home prices are going to appreciate 10% a year, then, honestly, the right answer is you should take on 100% debt," Rohde says. "The problem is, you don't know that for certain. And if you're a young person starting out, putting all of your eggs into that one basket is, financially, not a smart move."

The leaders of this new crop of startups understand what they're up against. Elbogen was formerly an executive at Unison, a company that tried to partner with homebuyers on their purchases before focusing on making investment deals with existing homeowners. Yes, Jubilee customers are responsible for the ongoing homeownership costs, and they're giving up a chunk of the home's future appreciation when they sign on to the deal. But they also have significant upside, he says — they're building home equity from day one, and they get the benefits of smaller down payments and monthly outlays. The most important part, Elbogen tells me, "is making sure that there's enough education and understanding to see what that trade-off is."

With home prices in many areas still at or near record highs, some buyers will inevitably seek alternate routes. Jackie Thompson, a 28-year-old laborer at a cement company, knew he wanted to buy a place in his hometown of Tehachapi, California, before home values there rose further out of reach: "I didn't want to get priced out of buying a home in the place that I grew up," he tells me. He has "decent credit" and good rental history, but a high debt-to-income ratio — he's paying off a car and a motorcycle, and his fiancée is busy raising their nine-year-old daughter. The lenders he surveyed would only pre-approve him for a maximum loan of roughly $260,000 loan, which wouldn't get him far in an area where the median home price is more than $400,000.

Then he saw an Instagram ad for Jubilee. An hour after he reached out to the company, he got a call from a representative who walked him through the leasehold concept. "When he explained it to me, it all seemed feasible," Thompson tells me. He was encouraged that he'd have the option to buy the land from Jubilee down the line. "That kind of set it for me," he adds.

Thompson and his fiancée are now under contract to purchase a three-bedroom home alongside Jubilee for a total of $300,000, with the land accounting for roughly 54% of the price. The goal, Thompson tells me, is to pay down the mortgage and eventually buy "more of a dream-home situation," with another bedroom and space to work on cars and motorcycles.

"This is my foot in the door," Thompson says.

James Rodriguez is a correspondent on Business Insider's Discourse team.

Popular Products

-

Fake Pregnancy Test

Fake Pregnancy Test$61.56$30.78 -

Anti-Slip Safety Handle for Elderly S...

Anti-Slip Safety Handle for Elderly S...$57.56$28.78 -

Toe Corrector Orthotics

Toe Corrector Orthotics$41.56$20.78 -

Waterproof Trauma Medical First Aid Kit

Waterproof Trauma Medical First Aid Kit$169.56$84.78 -

Rescue Zip Stitch Kit

Rescue Zip Stitch Kit$109.56$54.78