Why Do Older Sellers Get Less Money For Their Homes Than Younger Sellers?

Buying and selling a home can be the most significant financial decisions that families face.

For most Americans, buying and selling a home are the most significant financial decisions that families face over their lifetimes. Much research has focused on the buying side, primarily looking at how the availability and cost of mortgages vary by race and age. Much less research has examined the selling side. A recent study released by the Center for Retirement Research shows that older sellers earn lower returns.

More specifically, an 80-year-old seller realizes about 0.5 percent per year less than a 45-year-old, which corresponds to a 5-percent-lower sales price for a home with the mean U.S. holding period (11 years). On the typical home price of $400,000, this reduction amounts to a loss of $20,000. And the losses would be greater for older sellers. Two factors contribute to this outcome. First, homes sold by older people are less likely to be well-maintained. Second, older sellers are less likely to sell their homes through the Multiple Listing Services (MLS) and more likely to sell to investors.

Prior research has found that older people tend to realize lower returns when they sell their homes, but these studies often rely on self-reported home values. To get a more accurate and comprehensive analysis of age-related disparities required, the analysis starts by constructing a new dataset that links actual housing transactions in the CoreLogic Deeds database to ages in voter registration records.

CoreLogic aggregates public deed records from over 3,000 county clerk and recorder offices across the United States. CoreLogic also has a subset of transactions marketed through the MLS, which includes additional details such as the asking price, original listing date, and more property characteristics. The final sample for the baseline regression analysis consists of about 10 million repeat sales.

The baseline regression estimates the relationship between the average annual return on a house sale and the seller’s age. The equation includes information on: 1) zip-code location, buy year, sell year, and their interactions; 2) seller’s race, ethnicity, gender, and marital status; and 3) the age of the structure on the property, the holding period, and whether the event was a cash sale.

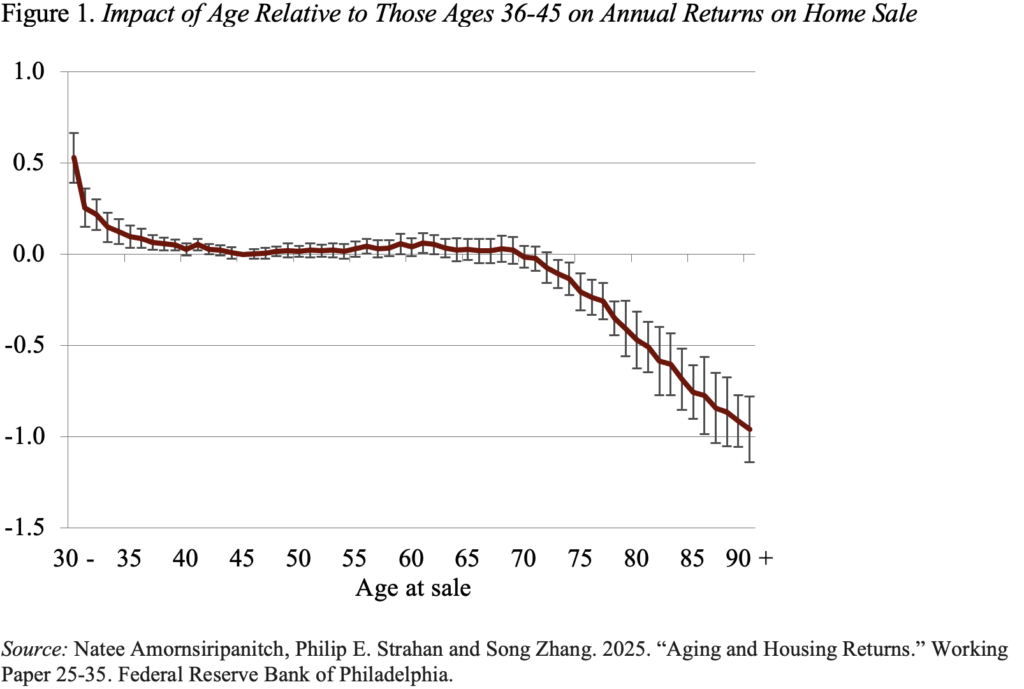

With the results from this base regression, it is possible to plot the annualized returns by seller age relative to returns of those ages 36-45. The decline in returns begins at age 70 and then accelerates thereafter (see Figure 1). The question is why?

To test whether the condition of the property helped explain the age gap in returns, the analysis focused on the sales offered through the MLS – where more details about the property are available. The researchers used the text description to construct four variables: “high positive,” where the text mentions major upgrades, such as a new roof or remodeled kitchen to “high negative,” where the text includes words like “fixer-upper” or “as-is.” In between were “low positive,” where the text mentioned minor cosmetic updates, such as fresh paint or finishes, and “neutral,” where the text included marketing terms, such as cozy, but no upgrades. Not surprisingly, the likelihood of high positive, low positive, and neutral descriptions declined throughout the life cycle, while the high negative category increased sharply among the oldest sellers.

Re-estimating the relationship between age and return for this subset of MLS transactions and adding the quality measures shows that both high positive and high negative ratings help explain the lower returns for older sellers.

The second possible explanation for the lower return for older sellers is how the transaction is managed. Properties sold via the MLS are advertised on a publicly available list and usually receive the market price. In contrast, properties sold privately have less exposure, and some agents may encourage their clients to sell to professional investors or developers so that they can receive higher fees. A pattern of older sellers more likely to sell off-MLS and/or to investors could explain why they end up with lower prices.

A simple regression showed that – including similar control variables as in prior regressions – the likelihood of private listings and sales to investors increases with age. And a final equation shows that sellers who market off-MLS or sell their properties to investors receive lower returns than sellers who go through the MLS.

With regard to the marketing issue, the study concludes with some good news – policy changes could help. Specifically, reforms introduced in Illinois to make private listings more transparent significantly reduced both the prevalence of private listings and the magnitude of the age gap.

Popular Products

-

Devil Horn Headband

Devil Horn Headband$25.99$11.78 -

WiFi Smart Video Doorbell Camera with...

WiFi Smart Video Doorbell Camera with...$61.56$30.78 -

Smart GPS Waterproof Mini Pet Tracker

Smart GPS Waterproof Mini Pet Tracker$59.56$29.78 -

Unisex Adjustable Back Posture Corrector

Unisex Adjustable Back Posture Corrector$71.56$35.78 -

Smart Bluetooth Aroma Diffuser

Smart Bluetooth Aroma Diffuser$585.56$292.87